Climate Conditionality and the Burden-Shift: Morocco’s IMF Resilience and Sustainability Facility as a Case Study in Green Colonialism

Shady Hassan, IFI Economics | For think tanks, civil society, and the IMF 2026 RSF Review

KEY MESSAGES

KEY MESSAGES

- The IMF’s Resilience and Sustainability Facility (RSF) in Morocco institutionalised the climate-justice deficit. Its original carbon-pricing measure — RM10, a regressive VAT on fossil fuels — was so socially toxic that Moroccan authorities refused to implement it and absorbed the withholding of SDR 62.5 million.

- Morocco’s negotiated replacement, RM17, taxed industrial polluters instead of households — and the IMF’s own CPAT modelling found its emissions impact in 2030 would be about 12 percent greater. The Fund’s default design failed; the country’s contextual knowledge succeeded.

- RM9, the economy-wide carbon tax, remains unimplemented. The IMF’s 2026 Article IV report continues to press for it. The pressure is not episodic; it is structural.

- RSF conditionality, EU CBAM compliance costs, and US IRA local-content subsidies together form a layered architecture that shifts the costs of the Global North’s transition onto a country whose per-capita emissions are roughly one-seventh those of the United States. This is green colonialism — quantifiable, and continuing.

- The Climate Justice Deficit, Operationalised

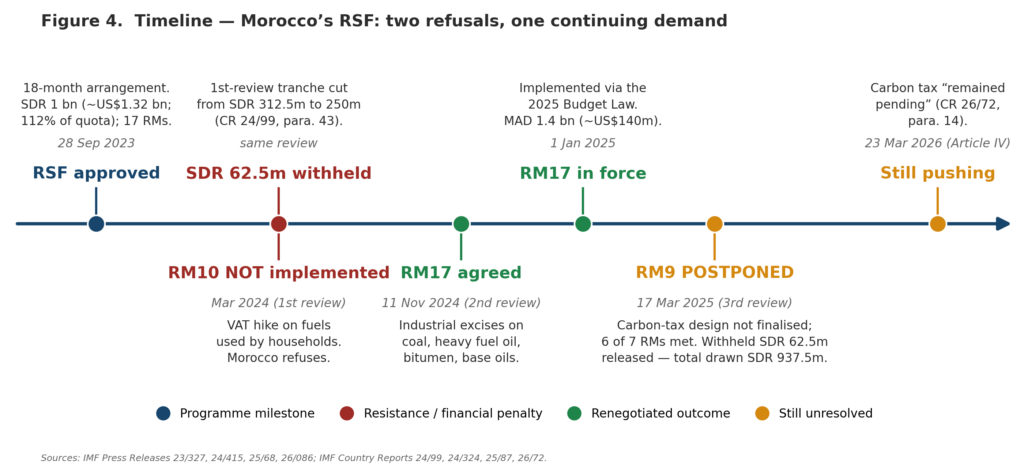

The IMF’s Resilience and Sustainability Facility (RSF), launched in 2022, was sold as a structural break with the institution’s history of austerity-driven adjustment. Morocco was an early signatory and was meant to be a showcase. The third and final review of its RSF concluded in March 2025, and the IMF’s 2026 Article IV report has now reviewed the country’s macroeconomic trajectory through the first quarter of 2026. Across this full cycle, two facts cut through the official record.

First, the only RSF conditionality the Moroccan authorities openly refused to implement — Reform Measure 10 (RM10), a gradual increase in the Value-Added Tax on fossil fuels from 10 to 20 percent — was refused on explicit social-cohesion grounds. The IMF’s own staff report records that the measure would “hurt households’ disposable income at a time when unemployment is high, food prices are still elevated, and the social protection regime is undergoing a deep structural change.”[1] Second, the only measure of the seven scheduled for the final review that was not implemented — Reform Measure 9 (RM9), the design of an economy-wide carbon tax — remains pending, and the IMF’s March 2026 Staff Report explicitly continues to push for its “design and implementation.”[2]

This brief argues that these two episodes are not isolated negotiating frictions. They are the visible surface of a structural feature of the RSF’s design: the systematic transfer of climate-adjustment costs from the Global North — which built its wealth on the carbon stock now destabilising the planet — onto the public budgets and household incomes of developing nations that contributed virtually nothing to the crisis. The framing is not rhetorical. It is documented in the IMF’s own modelling, in Morocco’s measurable emissions profile, and in the parallel architecture of EU and US climate policy.

The argument proceeds as follows. Section 2 grounds the climate-justice claim in the empirical asymmetry of per-capita emissions. Section 3 reconstructs the RM10 → RM17 substitution from IMF primary documents and shows what Morocco’s resistance demonstrates about feasible alternatives. Section 4 analyses the still-pending carbon tax and the IMF’s continuing pressure. Section 5 places the Moroccan case in the systemic context of EU CBAM and US IRA. Section 6 concludes with policy recommendations for civil society, Moroccan policymakers, and the IMF’s ongoing 2026 Review of Program Design and Conditionality.

- The Asymmetry the RSF Ignores

The principle of Common But Differentiated Responsibilities (CBDR), enshrined in Article 3(1) of the UNFCCC and reaffirmed in Article 2(2) of the Paris Agreement, is the legal floor of international climate law. It establishes that historical contribution to the crisis and current capacity to address it should govern the distribution of mitigation burdens. The empirical asymmetry is uncontested.

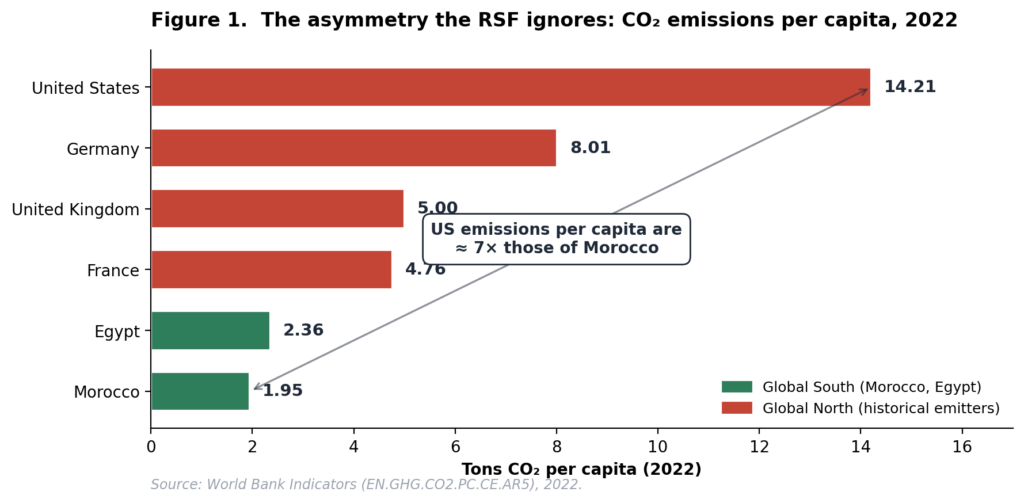

Figure 1. CO₂ emissions per capita, selected countries, 2022. Source: World Bank Indicators.[3]

An average resident of the United States emits roughly seven times as much CO₂ per year as an average Moroccan, and an average German emits four times as much. Yet the macroeconomic policy framework imposed on Morocco through the RSF requires the Moroccan state to legislate domestic carbon pricing — funded out of Moroccan household budgets and Moroccan firm balance sheets — as a precondition for accessing concessional climate finance. The Fund’s governance structure, weighted by financial quota rather than population or climate vulnerability, makes this asymmetry institutional rather than incidental.

This is the burden-shift in its clearest form. A crisis built on Northern emissions becomes a domestic fiscal problem for a Southern nation to solve under threat of withheld disbursements. The framing of “green colonialism” describes precisely this — the use of debt and conditionality to extract the financing of decarbonisation from the populations of low-emitting nations while the historical polluters retain policy autonomy over their own transition.

The asymmetry is cumulative as well as current, and it has been quantified. Hickel (2020), applying an equality-based attribution of the atmospheric commons in The Lancet Planetary Health, finds that the Global North is responsible for 92 percent of cumulative CO₂ emissions in excess of the 350-ppm planetary boundary — the United States alone for 40 percent — while most countries of the Global South remain within their fair shares.[4] The study grounds its attribution method explicitly in the CBDR principle. On any responsibility-based allocation of the remaining global mitigation effort, therefore, the near-term abatement obligation of a country emitting 1.95 tons of CO₂ per capita approaches zero. Every ton of abatement that conditionality compels Morocco to finance domestically is a ton that the economies which produced the excess did not have to abate at home.

Morocco’s own climate commitments already encode this fair-shares logic — and independent assessment confirms it. The 2021 updated NDC set a headline reduction of 45.5 percent below business-as-usual by 2030, of which only 18.3 percentage points are unconditional; the remaining 27.2 points are explicitly contingent on international support, with roughly US$21.5 billion of the programme’s US$38.8 billion cost to be internationally financed.[5] The Climate Action Tracker independently rates Morocco’s policies and unconditional target as meeting the country’s fair-share contribution to the 1.5°C limit.[6] The conditional tranche is thus Morocco’s declared statement of where its fair share ends and where the Global North’s treaty obligation — UNFCCC Article 4.3, Paris Agreement Article 9.1 — begins. The RSF inverts that architecture: it converts effort belonging to the conditional tranche into repayable, policy-conditioned debt, financed through Special Drawing Rights that wealthier members place with the Resilience and Sustainability Trust as remunerated loans, not grants. And the lever of the inversion is vulnerability itself. The countries most exposed to climate damage are precisely those most in need of climate finance, and it is that need — not any responsibility for the crisis — that conditionality monetises.

- Episode One: The Design Morocco Refused

3.1 What RM10 demanded

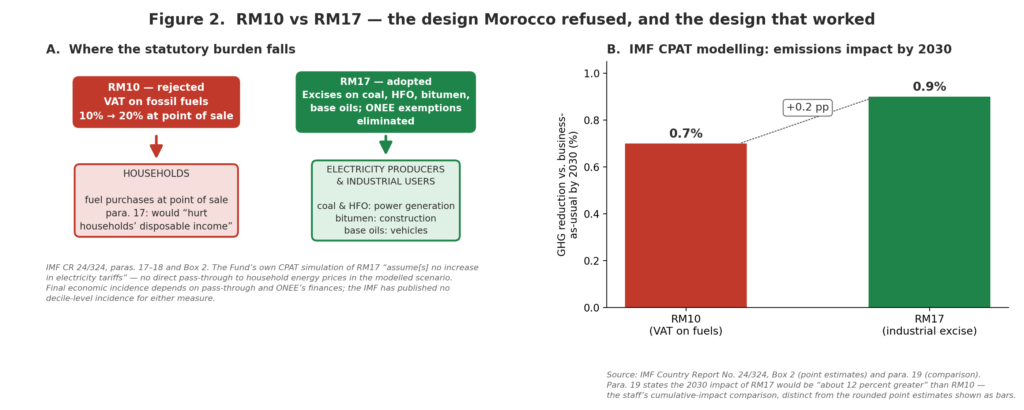

Approved on 28 September 2023, Morocco’s 18-month RSF arrangement provided SDR 1 billion (approximately US$1.32 billion, 112 percent of quota) against a programme of 17 Reform Measures. RM10 — the most fiscally consequential measure — required the Moroccan authorities to introduce, through the 2024 Budget Law, a gradual increase in the VAT on fossil fuels from 10 to 20 percent over ten years, eliminating the bulk of so-called “brown” tax expenditures.[7]

In macroeconomic terms, RM10 is a textbook regressive instrument. VAT applies uniformly at the point of sale regardless of income. Because demand for cooking fuel and transport fuel is largely inelastic for working-class households — there are no electrified buses to switch to in rural Morocco — fuel-price increases consume a disproportionate share of low-income budgets. The Fund’s price-elasticity logic assumes substitution. In Morocco’s actual economy, it produced compression: spending cuts on food, healthcare, and education to absorb a tax meant to address a problem the population had not caused.

3.2 The refusal and its cost

RM10’s macroeconomic moment could not have been worse. Morocco’s energy import bill had nearly doubled in 2022 to roughly MAD 153 billion — some 11–12 percent of GDP — after the commodity shock. The agricultural sector, traditionally the country’s largest employer, shed 137,000 jobs in 2024 alone as the latest in a succession of droughts — the fourth dry rain season in five years, by the IMF’s own count — pushed cereal production to roughly 31 million quintals — less than half the long-term average.[8] Unemployment held at 13 percent. Cost-of-living protests ran continuously through 2022 and 2023 in Casablanca, Rabat, Tangier, Agadir, and Meknes.

In this environment, the Moroccan Ministry of Economy and Finance refused to implement RM10 by the first review deadline. The IMF responded by withholding SDR 62.5 million of the scheduled disbursement — reducing the first-review payout from SDR 312.5 million to SDR 250 million. The coercive lever of climate conditionality became visible: a developing nation that prioritised the survival of its citizens over a regressive consumption tax was financially penalised by an international creditor.

“Increasing the VAT on fossil fuels … would hurt households’ disposable income at a time when unemployment is high, food prices are still elevated, and the social protection regime is undergoing a deep structural change.” — IMF Country Report 24/324, ¶17, reporting the Moroccan authorities’ rationale[9]

3.3 RM17: what Morocco built instead

By December 2024, the Moroccan authorities had negotiated a replacement. Reform Measure 17 (RM17), enacted in the 2025 Budget Law and effective 1 January 2025, abandoned the broad consumer VAT in favour of targeted increases in the Domestic Consumption Tax (TIC) on four polluting industrial inputs — coal, heavy fuel oil, bitumen, and base lubricating oils. Crucially, RM17 also eliminated the long-standing TIC exemptions that had been granted to the state utility ONEE and its concessionaires. The locus of the tax shifted from the household kitchen to the industrial boiler.

Figure 2. RM10 vs RM17 — statutory incidence of the two designs (panel A) and IMF-modelled emissions impact (panel B). Source: IMF CR 24/324, ¶¶17–19 and Box 2.

3.4 The data behind the substitution

Table 1 below sets out the specific TIC rate changes legislated under RM17 and effective from 1 January 2025.

| Polluting product | Previous TIC | New TIC (RM17) | Change |

| Coal | 64.80 DH / ton | 124.80 DH / ton | + 92.6 % |

| Heavy fuel oil | 182.40 DH / ton | 242.40 DH / ton | + 32.9 % |

| Bitumen | 45.00 DH / 100 kg | 51.00 DH / 100 kg | + 13.3 % |

| Lubricating oils (base) | 228.00 DH / 100 kg | 234.00 DH / 100 kg | + 2.6 % |

Table 1. Domestic Consumption Tax (TIC) rate changes legislated under RM17, effective 1 January 2025. Coal and heavy-fuel-oil rates from IMF CR 24/324, Box 2; bitumen and base-oil rates from Morocco’s Loi de Finances 2025.[10]

The IMF’s joint World Bank Climate Policy Assessment Tool (CPAT), calibrated to Moroccan household data, simulated both designs. Its conclusion is recorded verbatim in the Second Review staff report: the emissions impact of RM17 in 2030 would be “about 12 percent greater”[11] than the gradual VAT increase originally envisaged under RM10. The fiscal yield for 2025 alone was estimated at MAD 1.4 billion (~US$140 million). The withheld SDR 62.5 million was released alongside the third-review disbursement, bringing total RSF drawings to SDR 937.5 million (~US$1.24 billion).[12] The mechanism in the Fund’s own simulation is instructive. With roughly 80 percent of coal-fired generation locked into long-term take-or-pay contracts with independent producers, the modelled emissions effect comes almost entirely from ONEE switching its directly operated coal capacity to non-coal sources — and the simulation explicitly assumes no increase in electricity tariffs. On the IMF’s own assumptions, in other words, the replacement measure delivers the greater emissions impact without any direct pass-through to household energy prices.[13]

What the substitution proves is decisive for the climate-justice case. A more progressive design — taxing upstream polluters and removing industrial subsidies — produced better climate outcomes than a regressive consumer tax. The IMF’s default instrument was inferior on its own terms. Morocco demonstrated, against IMF pressure, that decarbonisation can be financed without compressing the budgets of people experiencing poverty. The IMF accepted the result only after withholding funds and only after the substitution was modelled to its satisfaction. Yet the substitution settled only the question of who within Morocco pays. The prior question — whether the Moroccan economy should have carried this abatement effort at all — was never on the table. That RM17’s proceeds accrue to the Moroccan treasury does not answer it: the burden at issue is not the fiscal flow but the mitigation effort itself — the real resources, industrial adjustment, and policy capacity that a low-emitting economy is compelled to commit, under threat of withheld disbursements, to a crisis generated overwhelmingly elsewhere (Section 2).

“In the current socioeconomic context with still elevated food prices and high unemployment, it appears more socially acceptable to pursue increases in excises on coal and other highly polluting products than a higher value-added tax (VAT) on fossil fuels.” — Kenji Okamura, IMF Acting Chair, Press Release 24/415, November 2024[14]

- Episode Two: The Carbon Tax the IMF Will Not DropThe third and final RSF review concluded on 17 March 2025. Of the seven Reform Measures scheduled for that review, six were implemented. The one that was not was Reform Measure 9 — the production and adoption of a design document for an economy-wide carbon tax.

“The RSF arrangement concluded with the implementation of six of the seven measures scheduled for the third and final review. … The gradual introduction of the carbon tax was not implemented as the authorities needed to undertake further analysis of its impact and deeper consultations with public and private stakeholders.” — IMF Press Release 25/68, 18 March 2025[15]

The Moroccan authorities’ Letter of Intent to the IMF (Fettah and Jouahri, February 2025) frames the postponement in language deliberately close to RM10’s: “Considering the relevant economic and social implications of the introduction of the carbon tax and attaching great importance to the success of this reform, the Government has decided to devote more time to finalizing the design document planned under RM9.”[16] The pattern is the same as the RM10 episode. Confronted with an instrument that would impose carbon costs directly on Moroccan firms and households, the authorities sought time, consultations, and the protection of their fiscal sovereignty.

What is new is what the IMF did next. With the RSF formally concluded and Morocco simultaneously moved onto a Flexible Credit Line arrangement, the carbon-tax pressure migrated out of the RSF framework and into the regular Article IV consultation process. The Fund’s 2026 Article IV report, published in March 2026, makes the continuation explicit.

“Staff also encouraged mobilization of additional revenue (including higher excises on tobacco and improved property taxation of real estate assets) and progress in the design and implementation of a carbon tax (reform measure under the Resilience and Sustainability Facility (RSF) that remained pending).” — IMF Country Report 26/72, ¶14, March 2026[17]

Two features of this continuing pressure deserve emphasis. The first is the framing. The IMF presents the carbon tax as a revenue-mobilisation instrument — alongside excises on tobacco and improvements in property taxation. The climate rationale, originally central to the RSF, has shifted to a fiscal-consolidation rationale. The carbon tax is now justified primarily by what it can raise for the Moroccan treasury, not by what it can do for global decarbonisation. The substantive question of who pays — Moroccan firms operating on tight margins in carbon-intensive sectors that are already losing competitiveness against subsidised Northern producers — is not addressed in the staff report’s recommendation.

The second feature is the absence of any reciprocal commitment from the Global North. The IMF demands a carbon tax from a country emitting 1.95 tons CO₂ per capita. It does not demand commensurate climate finance from the countries emitting 14.21.[18] It does not condition its lending to high-income members on decarbonisation timelines. The asymmetry of conditionality maps exactly onto the asymmetry of historical responsibility — inverted.

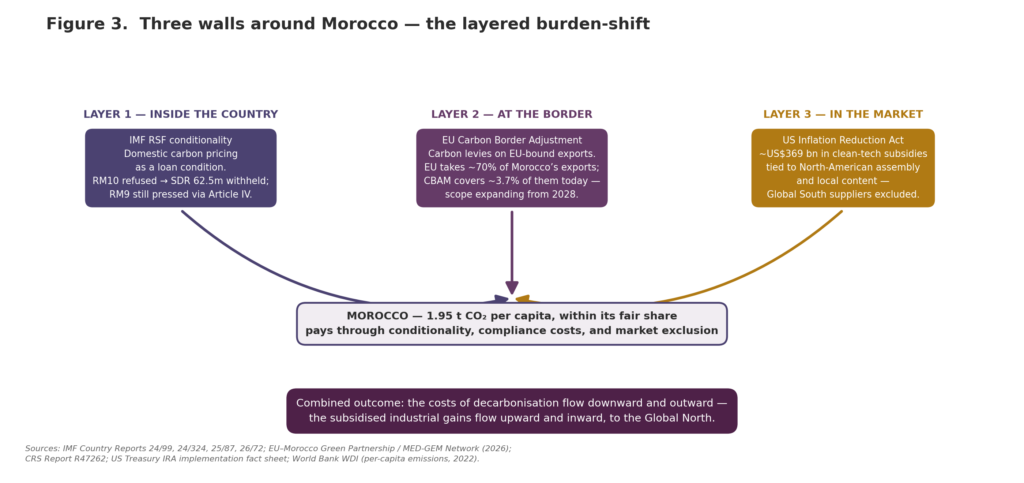

- Systemic, Not Episodic: Three Walls Around Morocco

Morocco’s experience under the RSF is a single instance of a broader policy architecture in which the Global North simultaneously subsidises its own clean-tech industries, imposes carbon costs at its borders on developing-country exports, and demands domestic carbon pricing inside developing countries through multilateral conditionality. Each instrument carries a defensible climate rationale in isolation. The composite system, however, has a clear distributional logic: the costs of decarbonisation flow downward and outward; the industrial gains flow upward and inward.

Figure 3. Three layers of the systemic burden-shift on Morocco

5.1 Layer one — the IMF inside the country

This is the case set out above: RM10’s withheld SDR 62.5 million, the negotiated RM17 substitution, and the continuing pressure on RM9. The instrument is conditionality. The lever is access to concessional finance. The cost falls on the Moroccan public budget and ultimately on Moroccan households and firms.

5.2 Layer two — the EU Carbon Border Adjustment Mechanism

The EU CBAM, which entered its definitive phase on 1 January 2026, imposes carbon-price-equivalent levies on imports of cement, iron and steel, aluminium, fertilisers, electricity, and hydrogen. Approximately 70 percent of Moroccan exports go to the European Union, and Morocco’s phosphate-fertiliser exports to the EU reached roughly US$2.5 billion in 2024. Precision matters here: in its opening configuration the mechanism’s covered products — mainly fertilisers and, to a lesser extent, cement — account for roughly 3.7 percent of Morocco’s EU-bound exports, a figure reported by the EU–Morocco Green Partnership’s own national CBAM workshop.UNCTAD modelling found that under its higher-carbon-price scenario the EU gains roughly US$5.9 billion in income while developing countries lose US$10.2 billion; under the lower-price scenario, developed countries collectively gain US$2.5 billion while developing countries still lose US$5.9 billion — the direction of the burden-shift is identical across specifications.[19] The exposure is structural rather than static, however: the European Commission proposed in December 2025 to extend the mechanism to some 180 downstream product categories from 2028; Morocco’s prospective green-hydrogen exports, destined entirely for the European market, will be covered in full; and because seven of every ten Moroccan export dirhams already go to the EU, each widening of scope operates on a trade relationship the country cannot diversify away from. [20] Peer-reviewed analysis (Sun et al., 2023) confirms that CBAM reduces global carbon leakage by only about 19 percent, while “the EU is the major beneficiary, enjoying a welfare increase of $2.6 billion, accounting for 73 percent of the total welfare gains due to the CBAM.”[21] The same paper concludes that CBAM “overburdens developing countries”[22] and that “wealthy countries as a group enjoy net benefits while the poor countries as a group suffer net losses.”

The World Bank’s World Development Report 2025 documents that compliance costs from non-tariff measures and product standards can reach up to US$425,000 per firm in developing nations.[23] The same report records that non-tariff measures — pesticide specifications, labelling requirements, product standards — now affect 90 percent of global trade, up from roughly 15 percent in the late 1990s.[24] As the author has argued elsewhere in The Invisible Trade Walls (Hassan, 2026), “compliance costs are becoming a structural subsidy paid by the Global South to maintain access to the Northern markets.”[25]

5.3 Layer three — the US Inflation Reduction Act

Where the EU imposes carbon costs on imports, the United States subsidises clean-tech production at home. The 2022 Inflation Reduction Act committed approximately US$369 billion as scored at enactment (with the credits largely uncapped, subsequent independent estimates range from roughly US$800 billion to US$1.2 trillion)[26] in tax credits and direct subsidies for clean energy, electric vehicles, and battery manufacturing — and tied the most valuable credits to North American assembly and rising local-content thresholds on critical minerals and battery components. The structural effect is to channel the capital expenditure of the global clean-tech transition into the United States and its FTA partners, while excluding suppliers from the Global South.

Considered together, the three layers form a closed system. The North subsidises its own green industries (IRA). It charges carbon at its borders to protect those industries (CBAM). And it uses multilateral institutions to require that developing countries impose carbon costs domestically as a condition of climate finance (RSF). At every layer, the bill is paid by the same parties: the public budgets and the productive sectors of countries that contributed least to the crisis.

Figure 4. Timeline of Morocco’s RSF — two refusals, one continuing demand.

- Recommendations

6.1 For the IMF, in advance of the 2026 Review of Program Design and Conditionality

- Treat broad-based consumption taxes on fuels as inadmissible RSF reform measures in low- and middle-income countries with high inflation, weak labour markets, and underdeveloped social protection systems. Morocco’s own substitution proves that progressive industrial-excise designs deliver superior climate outcomes.

- Disclose, in every RSF staff report, the modelled distributional incidence of each reform measure across income deciles. The CPAT framework is capable of producing this output; the staff reports currently do not present it.

- Cease the use of disbursement withholding to enforce climate conditionality. Treating the SDR 62.5 million withheld from Morocco as a precedent for coercive climate finance is incompatible with the RST’s stated purpose of supporting transitions, not penalising hesitancy.

- Adopt CBDR-RC as an operative design principle for RSF conditionality — not as a rhetorical reference. In practice, this means accepting that the speed and stringency of carbon pricing in a country emitting 1.95 tons CO₂ per capita cannot be the same as in a country emitting 14.21.

6.2 For Moroccan and other Global South policymakers

- Treat the RM10 → RM17 substitution as a documented blueprint. The institutional architecture that enabled it — domestic technical capacity, willingness to absorb a temporary disbursement cost, and a counter-proposal grounded in the IMF’s own modelling framework — is replicable in other countries facing analogous conditionality pressure.

- Refuse the framing of the carbon tax as a fiscal-revenue instrument disconnected from international climate finance. Any future Moroccan carbon-pricing legislation should be explicitly contingent on commensurate climate-finance commitments from the Global North, in line with the conditional structure of Morocco’s NDCs — the 2021 update and NDC 3.0 (2025), which conditions even the country’s 2040 coal phase-out on international support.[27]

- Pursue debt-for-climate swaps and Special Drawing Rights re-allocation as primary sources of climate finance — not new RSF-style conditional lending that compounds external debt while demanding domestic fiscal contraction.

6.3 For civil society and think tanks

- Build the empirical case that Northern climate policy — CBAM, IRA, RSF — operates as a single composite system whose distributional outcomes are the proper subject of public scrutiny, rather than three separate technical files.

- Frame compliance costs and conditionality-driven adjustment as climate reparations owed by the Global North, not as aid offered by it. The legal and ethical anchor is CBDR-RC; the empirical anchor is per-capita emissions data; the operational anchor is the Moroccan precedent.

- Demand transparency of methodology. The IMF’s CPAT modelling is opaque; its parameter choices materially shaped both the design of RM10 and its eventual substitution. Open access to the model, its data, and its scenarios is a precondition for meaningful public accountability of climate conditionality.

- Conclusion: The Pattern Is the Point

Morocco’s RSF was meant to be a success story. By the IMF’s preferred metrics — programme completion, fiscal consolidation, sovereign rating upgrade, GDP growth recovery to 4.8 percent in the first three quarters of 2025 — it is. But the story the IMF tells about Morocco omits its most instructive element. The Moroccan authorities refused the climate measure that would have hurt their citizens, accepted the financial cost of refusal, and negotiated a substitution that was simultaneously more progressive and more effective. The IMF resisted that substitution before accepting it. And, with the RSF concluded, the Fund is now pressing for the same kind of broad carbon-pricing instrument through the Article IV channel.

This is not a technical disagreement over instrument choice. It is a sustained, institutional preference for designs that shift adjustment costs from international creditors to domestic populations. When that preference is applied to a country whose per-capita emissions are one-seventh those of the United States, in the name of a global crisis it did not cause, the word for it is green colonialism. The label is not a slogan. It is a description of the documented mechanics. And its lever is vulnerability itself: the exposure that makes a country need climate finance is the same exposure that conditionality converts into leverage over its fiscal choices.

The Moroccan resistance is the counter-evidence. Better climate policy, financed by progressive instruments and shielded by social protection, is not only available — it is, on the IMF’s own modelling, superior. The barrier is not knowledge or capacity. The barrier is the political-economic design of the international financial system, and it can be changed.

References

Primary IMF sources

- IMF (2023). “IMF Executive Board Approves US$1.3 Billion Under the Resilience and Sustainability Facility Arrangement for Morocco.” Press Release No. 23/327, 28 September 2023. https://www.imf.org/en/news/articles/2023/09/28/pr-23327-imf-approves-1-3-billion-under-the-rsf-arrangement-for-morocco

- IMF (2024a). Morocco: 2024 Article IV Consultation and First Review under the Arrangement under the Resilience and Sustainability Facility. IMF Country Report No. 24/99, March 2024. https://www.imf.org/-/media/files/publications/cr/2024/english/1marea2024001.pdf

- IMF (2024b). Morocco: Second Review under the Arrangement under the Resilience and Sustainability Facility — Press Release; Staff Report; and Statement by the Executive Director for Morocco. IMF Country Report No. 24/324, November 2024. https://www.imf.org/-/media/files/publications/cr/2024/english/1marea2024002-print-pdf.pdf

- IMF (2024c). “IMF Executive Board Concludes Second Review Under the Arrangement Under the Resilience and Sustainability Facility for Morocco.” Press Release No. 24/415, 12 November 2024. https://www.imf.org/en/news/articles/2024/11/12/pr-24415-morocco-imf-concludes-2nd-review-under-the-arrangement-under-the-rsf

- IMF (2025a). “IMF Executive Board Concludes 2025 Article IV Consultation, Third Review under the Resilience and Sustainability Facility with Morocco.” Press Release No. 25/68, 18 March 2025. https://www.imf.org/en/news/articles/2025/03/18/pr-2568-morocco-imf-concludes-2025-art-iv-consult-3rd-review-under-rsf

- IMF (2025b). Morocco: 2025 Article IV Consultation and Third Review under the Arrangement under the Resilience and Sustainability Facility — Press Release; Staff Report; and Statement by the Executive Director for Morocco. IMF Country Report No. 25/87, April 2025. https://www.elibrary.imf.org/view/journals/002/2025/087/article-A001-en.xml

- IMF (2026a). Morocco: 2026 Article IV Consultation and Review Under the Flexible Credit Line Arrangement — Press Release; Staff Report; and Statement by the Executive Director for Morocco. IMF Country Report No. 26/72, March 2026. https://www.elibrary.imf.org/view/journals/002/2026/072/article-A001-en.xml

- IMF (2026b). “IMF Executive Board Concludes 2026 Article IV Consultation, and Mid-Term Review Under the Flexible Credit Line Arrangement with Morocco.” Press Release No. 26/086, 23 March 2026. https://www.imf.org/en/news/articles/2026/03/23/pr26086-morocco-imf-concludes-2026-aiv-consultation-and-mid-term-rev-under-fcl-arrangement

Secondary sources

- Hassan, S. (2025). “The IMF and World Bank’s Grip on MENA — Background Paper.” MENAFem Movement, December 2025. https://menafemmovement.org/wp-content/uploads/2025/12/The-IMF-World-Banks-Grip-on-MENA.pdf

- Hassan, S. (2026). “The Invisible Trade Walls: How Climate Standards Shift Decarbonization Costs to Developing Nations.” Badr University in Cairo, April 2026. https://buc.edu.eg/wp-content/uploads/2026/04/Trade-walls.pdf

- Hassan, S. (2025). “Morocco’s Resistance: How a Nation Challenged the IMF on Climate Justice.” IFI Economics, Upcoming Research. https://ifi-economics.com/upcoming-research/morocco_RSF.html

- Sun, X., Mi, Z., Cheng, L., Coffman, D., & Liu, Y. (2023). “The carbon border adjustment mechanism is inefficient in addressing carbon leakage and results in unfair welfare losses.” Fundamental Research, 4(3), 660–670. https://pmc.ncbi.nlm.nih.gov/articles/PMC11630705/

- UNCTAD (2021). A European Union Carbon Border Adjustment Mechanism: Implications for developing countries. UNCTAD/OSG/INF/2021/2. https://unctad.org/system/files/official-document/osginf2021d2_en.pdf

- World Bank Group. World Development Indicators — CO₂ emissions per capita (EN.GHG.CO2.PC.CE.AR5). https://data.worldbank.org/indicator/EN.GHG.CO2.PC.CE.AR5

- Haut-Commissariat au Plan (HCP), Royaume du Maroc (2025). Note d’information sur la situation du marché du travail en 2024. https://www.hcp.ma

- United Nations Framework Convention on Climate Change (1992), Article 3(1); Paris Agreement (2015), Article 2(2). The principle of Common But Differentiated Responsibilities and Respective Capabilities.

- World Bank (2025). World Development Report 2025: Standards for Development. Washington, DC: World Bank, December 2025. https://www.worldbank.org/en/publication/wdr2025

- Congressional Research Service (2022). Inflation Reduction Act of 2022 (IRA): Provisions Related to Climate Change, CRS Report R47262; US Department of the Treasury, Fact Sheet: Implementing the Inflation Reduction Act’s Climate and Clean Energy Tax Incentives. https://home.treasury.gov/system/files/136/FactSheet-Implementing-IRA-Climate-CleanEnergy-TaxIncentives.pdf

- Hickel, J. (2020). “Quantifying national responsibility for climate breakdown: an equality-based attribution approach for carbon dioxide emissions in excess of the planetary boundary.” The Lancet Planetary Health, 4(9), e399–e404. https://www.thelancet.com/journals/lanplh/article/PIIS2542-5196(20)30196-0/fulltext

- Kingdom of Morocco (2021). Contribution Déterminée au Niveau National — actualisée (updated NDC), June 2021. UNFCCC NDC Registry. https://unfccc.int/sites/default/files/NDC/2022-06/Moroccan%20updated%20NDC%202021%20_Fr.pdf

- Kingdom of Morocco (2025). Nationally Determined Contribution 3.0. UNFCCC. https://unfccc.int/documents/497685

- Climate Action Tracker. Morocco country assessment. https://climateactiontracker.org/countries/morocco/

- UNEP NDC Action Project. Morocco country page (NDC implementation cost estimates). https://www.unep.org/ndc/action-area/morocco

- MED-GEM Network / EU–Morocco Green Partnership (2026). “CBAM in Morocco: A Strategic Workshop to Move from the Transitional Phase to Operationalisation.” February 2026. https://med-gem.eu/MoroccoCBAM

- European Commission, DG Taxation and Customs Union. Carbon Border Adjustment Mechanism (definitive regime from 1 January 2026). https://taxation-customs.ec.europa.eu/carbon-border-adjustment-mechanism_en

- Bachegour and Temmam (2026). “Morocco’s climate policy at a turning point under the EU CBAM.” NUPI Policy Brief 2/2026, Norwegian Institute of International Affairs. https://www.nupi.no/content/pdf_preview/31335/file/NUPI_Policy_brief_2026_2_Bachegour_Temmam.pdf

[1] IMF (2024), Country Report No. 24/324 (Second Review under the RSF), para. 17, p. 11.

[2] IMF (2026), Country Report No. 26/72 (2026 Article IV), para. 14.

[3] World Bank, World Development Indicators, CO2 emissions per capita (series EN.GHG.CO2.PC.CE.AR5), 2022 data.

[4] Hickel, J. (2020), “Quantifying national responsibility for climate breakdown,” The Lancet Planetary Health 4(9): e399–e404 (Reference 19). The United States accounts for 40 percent of excess emissions and the EU-28 for 29 percent. An update of the underlying dataset through 2019 places the Global North’s collective share at 86 percent (Global Inequality Project, 2025); the scale and direction of the attribution are unchanged.

[5] Kingdom of Morocco (2021), Contribution Déterminée au Niveau National — actualisée, June 2021 (Reference 20). Implementation cost estimates — US$38.8 billion in total, of which about US$21.5 billion to be financed with additional international support — per the UNEP NDC Action Project country assessment (Reference 23).

[6] Climate Action Tracker, Morocco country assessment (Reference 22): Morocco’s “policies and unconditional target meet its fair-share contribution” to limiting warming to 1.5°C.

[7] IMF (2023), Press Release No. 23/327; programme size and quota share also in IMF (2024), Country Report No. 24/324, Table 3, p. 19.

[8] Haut-Commissariat au Plan (2025), Note d’information sur la situation du marché du travail en 2024 (annual labour-market report): the agricultural sector lost 137,000 jobs in 2024 as a result of the drought. The World Bank RSF Assessment Letter in IMF CR 24/324 separately reports 141,000 rural jobs lost on a year-on-year basis in Q2 2024; the two figures measure different periods and categories.

[9] IMF (2024), Country Report No. 24/324, para. 17, p. 11.

[10] IMF (2024), Country Report No. 24/324, Box 2, p. 12 (coal and heavy-fuel-oil rates); bitumen and base-oil rates from Morocco’s Loi de Finances 2025 (cf. Memorandum of Economic and Financial Policies, ibid., para. 11, p. 56).

[11] IMF (2024), Country Report No. 24/324, para. 19, p. 11.

[12] IMF (2025), Country Report No. 25/87 (Third Review), para. 33, p. 24 (fiscal yield about MAD 1.4 billion); total RSF drawings of SDR 937.5 million confirmed in IMF (2025), Press Release No. 25/68.

[13] IMF (2024), Country Report No. 24/324, paras. 18–19 and Box 2, pp. 11–12. The simulation applies the coal price elasticity only to the roughly 20 percent of coal-fired generation produced directly by ONEE and states: “Lastly, we assume no increase in electricity tariffs.”

[14] IMF (2024), Press Release No. 24/415, 12 November 2024 (statement of Kenji Okamura, Acting Chair).

[15] IMF (2025), Press Release No. 25/68, 18 March 2025 (statement of Kenji Okamura, Acting Chair).

[16] IMF (2025), Country Report No. 25/87, Letter of Intent (Fettah and Jouahri), p. 69; the postponement is also recorded in the staff report, para. 34, p. 24.

[17] IMF (2026), Country Report No. 26/72, para. 14.

[18] World Bank, World Development Indicators, CO2 emissions per capita (series EN.GHG.CO2.PC.CE.AR5).

[19] CBAM coverage share (~3.7 percent of Morocco’s EU-bound exports, mainly fertilisers and cement): EU–Morocco Green Partnership national CBAM workshop, MED-GEM Network, February 2026 (Reference 24). Scope expansion (some 180 downstream product categories from 2028, proposed December 2025): European Commission (Reference 25). Hydrogen coverage and sectoral shares: Bachegour and Temmam (2026), NUPI Policy Brief 2/2026 (Reference 26). EU export-share figure (70.5 percent) per EU Commission data.

[20] UNCTAD (2021), A European Union Carbon Border Adjustment Mechanism: Implications for Developing Countries, p. 21, Table 6. CBAM-88 scenario: European Union +US$5,929 million; developing countries −US$10,208 million. CBAM-44 scenario: developed countries +US$2.5 billion; developing countries −US$5.9 billion.

[21] Sun et al. (2023), p. 665.

[22] Sun et al. (2023), p. 660 (“overburdens developing countries”) and p. 668 (“wealthy countries as a group enjoy net benefits while the poor countries as a group suffer net losses”).

[23] World Bank (2025), World Development Report 2025: Standards for Development (Reference 17); the US$425,000-per-firm compliance-cost figure as cited in Hassan (2026), The Invisible Trade Walls (Reference 10).

[24] World Bank (2025), World Development Report 2025: Standards for Development (Reference 17); figures as stated in the World Bank press release of 11 December 2025 accompanying the report.

[25] Hassan, S. (2026), The Invisible Trade Walls (Reference 10).

[26] US$369 billion is the climate-related score at enactment (see CRS Report R47262 and the US Treasury implementation fact sheet, Reference 18). Because the IRA’s principal tax credits are uncapped, subsequent estimates by Goldman Sachs, Brookings, and the US Treasury place the eventual fiscal cost between roughly US$800 billion and US$1.2 trillion.

[27] Kingdom of Morocco (2025), NDC 3.0 (Reference 21): the 2040 coal phase-out is conditional on international support, with an unconditional commitment to phase out in the 2040s.

ABOUT THE AUTHOR — Shady Hassan is the lead economic researcher at the Center for Global Affairs at Badr University in Cairo and is Principal Investigator of the IFI Economics research project of the MENAFem Movement for Economic, Development and Ecological Justice. This brief is grounded exclusively in primary institutional documents. [email protected];[email protected]